Atlasimmobilier practical guide – Real estate taxation in Morocco

Sellers often ask: “How much tax will I have to pay if I sell my property in Morocco? The answer can be summed up in three letters: TPI, or taxe sur le profit immobilier, a tax that’s simple to calculate but important to anticipate. Here are the essentials for understanding how it works, estimating the amount and optimizing your resale operation.

What is TPI in Morocco?

TPI is the tax levied by the Moroccan tax authorities on capital gains realized on the resale of a property. It applies to both individuals and companies, and is one of the main taxes to be taken into account when selling a property.

It applies whenever the sale price exceeds the revalued acquisition price. If there is no capital gain, only a minimum contribution of 3% is due.

How is TPI calculated? – A very simple mechanism

The calculation has a clear and transparent basis:

The acquisition cost corresponds to:

- to the purchase price of the property;

- increased by flat-rate acquisition costs of 15% (or the actual documented costs).

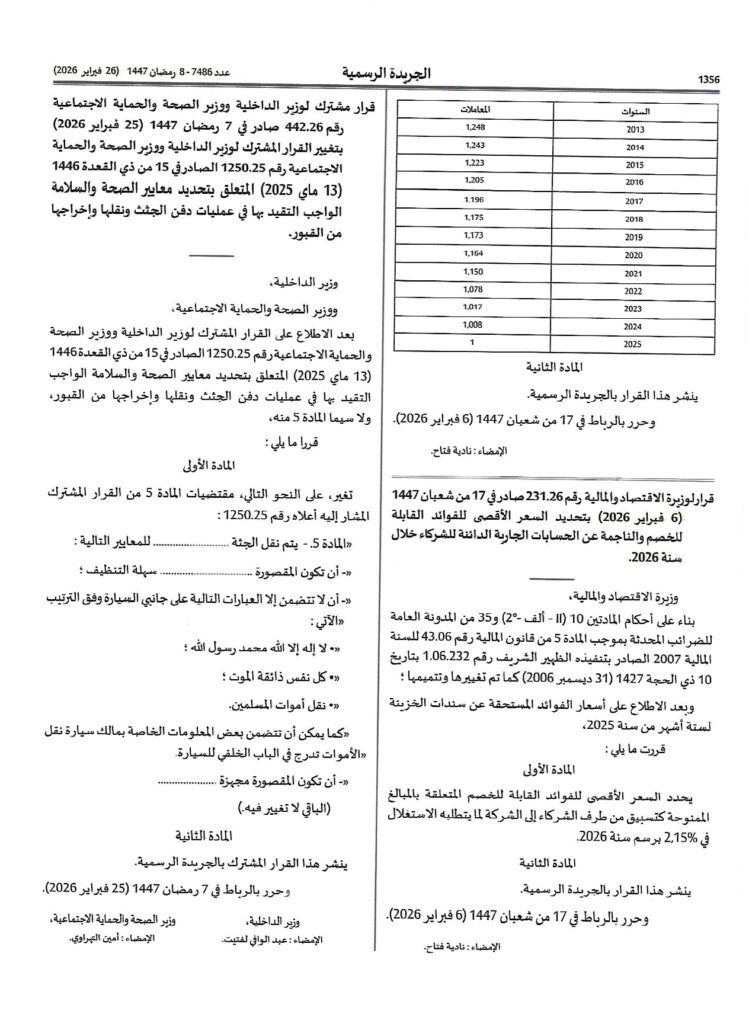

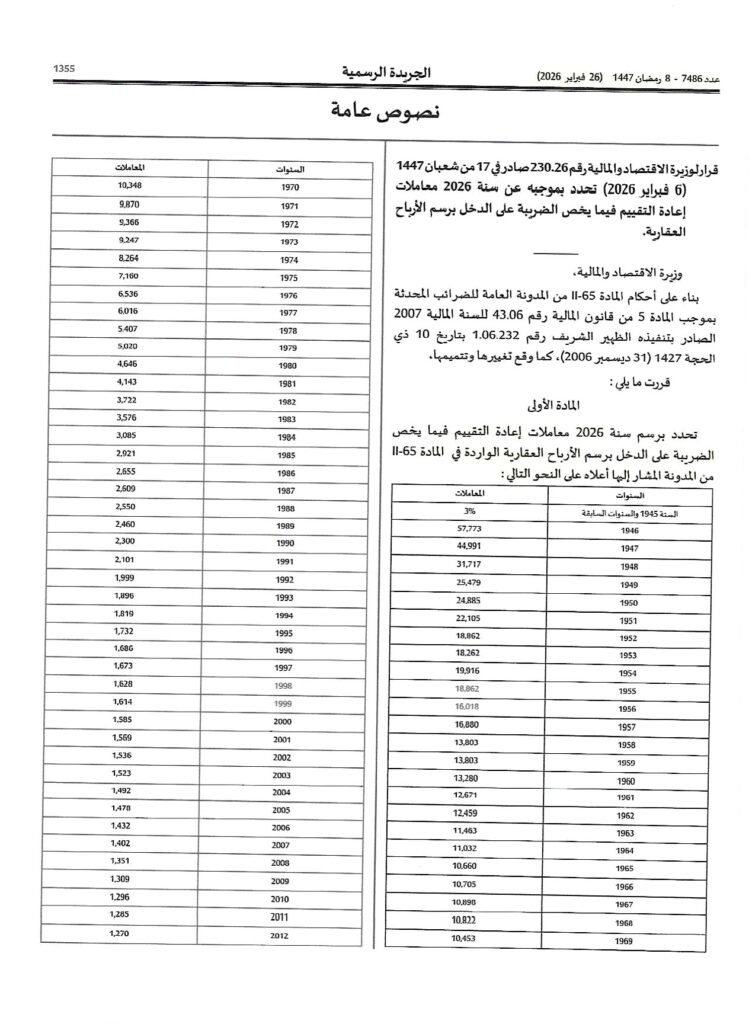

This acquisition cost is then multiplied by the revaluation coefficient published each year by the tax authorities. (See the 2026 table below)

The difference between the actual selling price and this revalued acquisition cost constitutes the taxable capital gain.

If this capital gain is positive, it is generally taxed at 20%.

However, the tax due cannot be lower than the minimum contribution of 3% of the selling price.

Simplified calculation example

You purchased a property for MAD 1,000,000 ten years ago (in 2016).

- Acquisition price: MAD 1,000,000

- Flat-rate acquisition costs (15%): MAD 150,000

- Acquisition cost retained: MAD 1,150,000

- Revaluation coefficient: 1.205

Revalued acquisition cost:

1,150,000 × 1.205 = MAD 1,385,750

Selling price: MAD 1,800,000

Taxable capital gain:

1,800,000 – 1,385,750 = MAD 414,250

Theoretical TPI:

20% × 414,250 = MAD 82,850

Minimum contribution:

3% × 1,800,000 = MAD 54,000

The TPI due will therefore amount to MAD 82,850.

Requesting prior administrative approval

Since July 1, 2023, it has been possible – and often recommended – to request a prior opinion from the tax authorities on the estimated amount of the TPI. This request must be made within 30 days of signing the preliminary sales agreement.

This notice makes it possible to anticipate precisely the amount to be paid, and avoid unpleasant surprises when the final deed is signed.

Payment of TPI: a discharge obligation

TPI is paid at the time of sale, generally through the notary. It is a final payment, meaning that once it has been paid, no subsequent adjustment can be claimed on the same profit.

Exceptions and special cases

Certain situations benefit from total or partial exemptions, in particular:

- Sale of a principal residence occupied for more than 6 years;

- The sale of an asset with a value below a certain threshold;

- Free transfers under certain family conditions.

On request, Atlasimmobilier can provide you with a personalized estimate of your TPI based on your property, your ownership history and the applicable tax regimes.

Atlasimmobilier Advice

Anticipating TPI is an essential step in your resale strategy. Our team can help you :

- Calculate your capital gain and the tax due;

- Optimize tax timelines (e.g. request for prior notice) ;

- Structuring the transaction to minimize tax risks.

FAQ – Morocco Capital Gains Tax (TPI) 2026

1. When do I have to pay TPI?

When the final deed of sale is signed, usually by a notary.

2. Can I be exempted?

Yes, especially if the property has been your principal residence for more than 5 years.

3. What happens if I lose money on resale?

If no capital gains are realized, only the minimum contribution of 3% of the sale price is due.

4. Can I contest the amount calculated by the administration?

Yes, in particular by requesting prior notice within 30 days of the compromise.

2026 Moroccan real estate revaluation coefficient: